Life insurance is one of the smartest ways to protect your family’s future. If something unexpected happens to you, the right policy can help your loved ones pay bills, cover daily expenses, and stay financially secure.

Many people know they need this insurance policy, but they are not sure how much coverage to buy. Too little may not fully protect your family, while too much can stretch your budget. The good news is that finding the right amount is simpler than it seems.

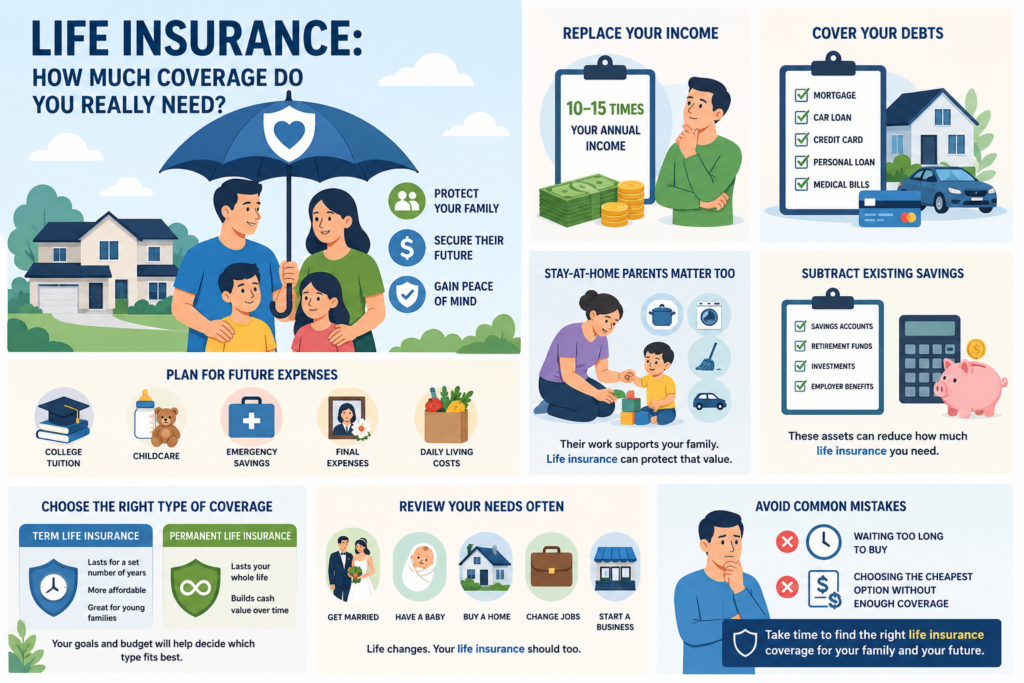

Why Life Insurance Matters

Life insurance gives your loved ones money after you pass away. That money can help cover daily bills, debts, and future costs. It can also give your family time to adjust without financial panic.

Many families depend on one or two incomes. If one income stops, the household may struggle. It helps replace that lost support.

Start With Your Income

A common rule is to buy coverage equal to 10 to 15 times your yearly income. For example, if you earn $50,000 a year, you may need $500,000 to $750,000 in life insurance.

This rule is only a starting point. Your real needs may be higher or lower depending on your family size, debts, and future plans.

Add Up Your Debts

Think about what your family would owe if you passed away today. Include:

- Mortgage balance

- Car loans

- Credit card debt

- Personal loans

- Medical bills

Your insurance policy can help your family pay these bills and avoid losing their home or savings.

Plan for Future Expenses

Your family may face major costs in the years ahead. Consider:

- Childcare

- College tuition

- Emergency savings

- Final expenses

- Daily living costs

When choosing this insurance, include these future needs so your family has long-term support.

Think About Stay-at-Home Parents Too

Even if someone does not earn a paycheck, their work has value. Childcare, cooking, cleaning, and transportation all cost money to replace.

A stay-at-home parent may also need life insurance because their role supports the whole household.

Subtract Existing Savings

You may already have money that can help your family, such as:

- Savings accounts

- Retirement funds

- Investments

- Employer benefits

These assets can reduce how much life insurance you need. Still, be careful not to depend only on savings.

Choose the Right Type of Life Insurance Coverage

There are two common options:

Term Coverage

Term life insurance lasts for a set number of years, such as 10, 20, or 30 years. It often costs less and works well for young families.

Permanent Coverage

Permanent life insurance can last your whole life as long as payments continue. It may build cash value over time.

Your goals and budget will help decide which type fits best.

Review Your Life Insurance Needs Often

Your coverage should change as life changes. Review your insurance policy when you:

- Get married

- Have a baby

- Buy a home

- Change jobs

- Start a business

A policy that fit five years ago may not fit today.

Avoid Common Mistakes

Many people wait too long to buy this. Others choose the cheapest option without enough coverage.

Do not guess. Take time to calculate your needs. The right life insurance plan should protect your family and fit your budget.

Life Insurance Final Thoughts

So, how much life insurance do you really need? The answer depends on your income, debts, future goals, and family needs. A smart policy can give peace of mind and financial security.

If you are unsure where to start, speak with a licensed agent. The right insurance amount today can make a huge difference tomorrow. Call Path Financial and Insurance today and ask us how!

You may also visit these links to get your quote: